The enactment of Sec. 199A provides one more reason to advise clients to create separate trusts for individual beneficiaries instead of a single trust. A single trust for the benefit of all the children may seem fair and less expensive when children are young. However, different ages, family size, economic status, and risk tolerance can create family tension when everyone is drawing from the same pot of money. Family tension and other nontax factors are reasons to set up separate trusts for each child and allow for those trusts to create separate subtrusts for future generations.

Two or more trusts are treated as one trust if they have substantially the same grantor or grantors and substantially the same primary beneficiary or beneficiaries, and a principal purpose of the trusts is the avoidance of federal income tax (Sec. 643(f)). However, in IRS Letter Ruling 199912034, the Service ruled that if a trust is divided into subtrusts and each subtrust has a different primary beneficiary, each subtrust will be treated as a separate trust for federal income tax purposes. Even though Prop. Regs. Sec. 1.643(f)-1 creates a presumption of tax avoidance if separate trusts create a significant income tax benefit, the test of primary beneficiaries being the same is still required for aggregation of trusts. Therefore, the creation or partition of trusts for separate beneficiaries should not violate Sec. 643(f).

Sec. 199A creates a qualified business income (QBI) deduction for taxpayers other than corporations. Under Sec. 199A, the “combined qualified business income amount” is the sum of the Sec. 199A(b)(2) amounts plus 20% of the aggregate amount of qualified real estate investment trust dividends and qualified publicly traded partnership income. The Sec. 199A(b)(2) amount is 20% of the QBI for each trade or business if the taxpayer’s taxable income is under the threshold (Sec. 199A(b)(3)(A)). Taxable income of a nongrantor trust, for the purpose of determining whether the trust exceeds the threshold amount, is determined before the distribution deduction and exemption amount (Prop. Regs. Sec. 1.199A-6(d)(3)(iii)).

The threshold for nongrantor trusts is $157,500, indexed for inflation after 2018 (Secs. 199A(b)(3) and 199A(e)(2)). If the taxpayer’s income exceeds the threshold, the Sec. 199A(b)(2) amount is the lesser of (1) 20% of the QBI for each trade or business or (2) the greater of (a) 50% of the W-2 wages of the qualified trade or business or (b) the sum of 25% of the wages of the qualified trade or business plus 2.5% of the unadjusted basis immediately after acquisition of all qualified property. The deductible amount is the combined QBI amount, limited to 20% of the excess (if any) of the taxpayer’s taxable income for the tax year over the taxpayer’s net capital gain for that tax year.

The following example shows the tax savings that can be gained through the creation of subtrusts when a single trust has QBI but the Sec. 199A deduction is limited by the Sec. 199A(b)(2)(B) limitation of wages or wages and unadjusted basis.

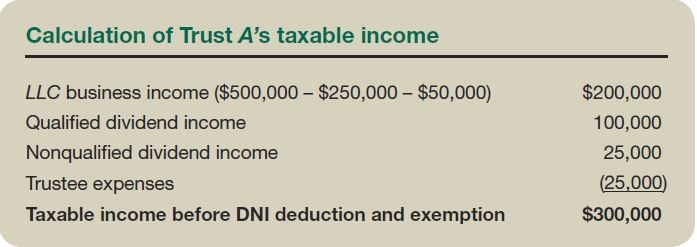

Example 1: Trust A has two beneficiaries, B and C. Trust A owns 100% of LLC, which operates the family business. The family business is not a specified service trade or business. LLC has revenue of $500,000, expenses of $250,000 excluding depreciation and wages, wage expense of $50,000, and depreciation expense of $25,000. The qualified property of LLC has $100,000 of unadjusted basis immediately after acquisition. Trust A also has qualified dividend income of $100,000, nonqualified dividend income of $25,000, and deductible indirect trustee expenses of $25,000.

Trust A calculates its taxable income for Sec. 199A as shown in the table below, “Calculation of Trust A’s Taxable Income.”

Since Trust A’s taxable income before the distributable net income (DNI) deduction and exemption exceeds the threshold amount of $157,500, Trust A is subject to the Sec. 199A(b)(2)(B) limitation of wages or wages and unadjusted basis. The Sec. 199A(b)(2)(B) limitation is $25,000, which is the greater of (1) 50% of $50,000 = $25,000, or (2) 25% of $50,000 plus 2.5% of $100,000 = $15,000.

Trust A calculates LLC’s QBI as shown in the table below, “Calculation of LLC’s QBI.”

Trust A’s deductible amount of LLC’s QBI is $25,000 (the lesser of 20% of $175,000 = $35,000, or the Sec. 199A(b)(2)(B) limitation of $25,000). Note that the depreciation deduction is allocated to the current income beneficiaries and is not considered when computing taxable income (Sec. 642(e)). However, under Prop. Regs. Sec. 1.199A-6(d)(3), any depletion and depreciation deductions described in Sec. 642(e) and any amortization deductions described in Sec. 642(f) that otherwise are properly included in the computation of QBI are included in the computation of QBI of the trust or estate regardless of how those deductions may otherwise be allocated between the trust or estate and its beneficiaries for other purposes of the Code.

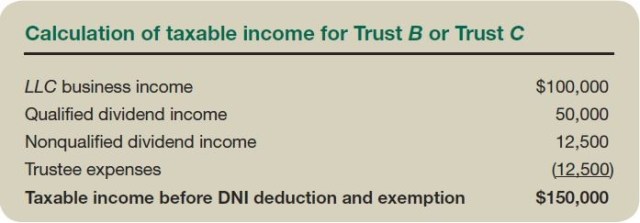

Alternatively, if Trust A is divided into Trust B for Beneficiary B and Trust C for Beneficiary C, and assets are split evenly into the two trusts, the calculations of taxable income for Trust B and for Trust C would be as shown in the table below, “Calculation of Taxable Income for Trust B or Trust C.”

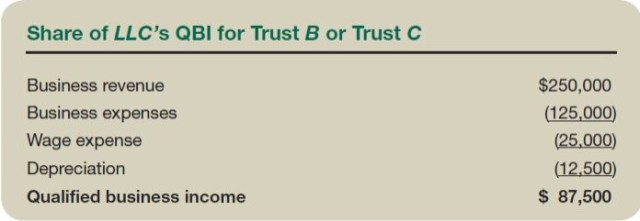

Trust B and Trust C calculate their share of LLC’s QBI as shown in the table below, “Share of LLC’s QBI for Trust B or Trust C.”

Since the taxable income is below the threshold amount, the deductible amount of LLC’s QBI for Trust B and Trust C is 20% of $87,500, or $17,500 each, for a total QBI deduction of $35,000.

Given that there are many nontax reasons to establish separate trusts for each beneficiary, advisers should consider the potential tax savings of a higher Sec. 199A deduction when trusts are being established or partitioning is being considered.